No other number unlocks doors of opportunities like your credit score. From gaining access to lower interest rates and better borrowing terms to better credit cards and exclusive perks, as well as insurance discounts and better rental options. Key to all these is having a good credit score.

What’s a credit score?

Your three-digit credit score speaks volumes about your creditworthiness. Lenders – mortgage bankers, credit card companies, auto dealers – check your credit score, along with your employment history and proof of income before they approve of your loan. The same is true with insurance companies and landlords who ascertain your financial responsibility before they issue you a policy or rent out a home.

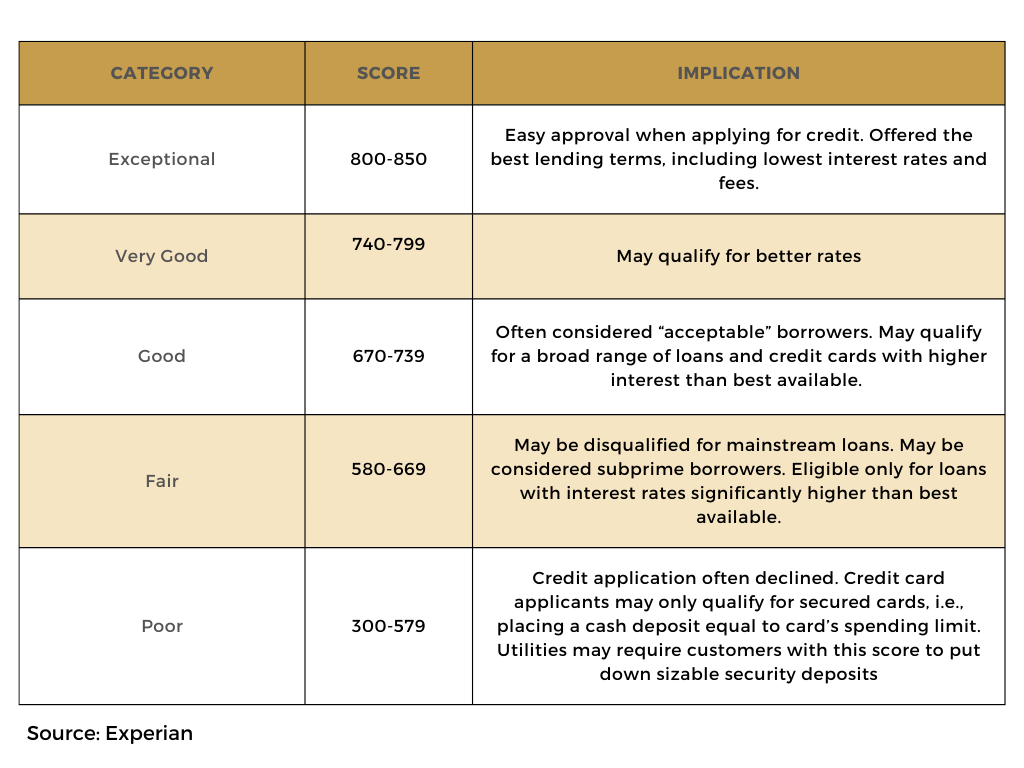

Implications per category

While there are many credit scoring models – which result in different credit scores –FICO Scores are used by 90% of top lenders. Ranging from 300 to 850, the higher your FICO score the better; it gives you better access to credit products at low interest rates. Different creditors have different standards for an acceptable score. Below is a general guideline:

Credit scores are calculated based on information about your credit accounts. Behind this data gathering are credit bureaus of which Equifax, Experian and TransUnion are the largest.

Factors behind the credit score

To improve your credit score, find out what factors influence your score and how to make these work for you.

- Payment history – The single biggest factor (35%) that affects your credit score is the timely payment of your bills. Remember: late payment that’s 30 days or more past the due date could drop your score by as much as 100 points.

- Credit utilization – The second biggest factor (30%) is your credit usage. To improve your credit score, experts recommend using less than 30% of your total credit card borrowing limit.

- Length of credit history – The age of your credit history is important (15%). If you must close credit accounts, close newer ones.

- New credit – Applying for a new credit (10%) triggers a hard inquiry on your credit report which in turn may result in a dip in your credit score. While the impact of these inquiries is small and short-lived, having too many at a short time can significantly lower your credit score.

- Credit mix – Having more than one type of credit (10%) ups your credit score. When you have a diverse credit portfolio – a mix of revolving accounts such as credit cards and installment accounts like auto loans and mortgage – it shows that you can handle different types of multiple loans.

Other steps to improve your credit score

Apart from managing your credit responsibly, take a pro-active approach to monitoring your credit accounts and paying off your debt by doing the following:

- Review your credit report - Request for one free credit report from each of the credit bureau every 12 months. Alert the credit bureaus for any errors.

- Set payment reminders – Never miss out on paying bills by writing deadlines on paper or online. By consistently paying your bills on time, your score can go up within a few months.

- Pay your balances in full – If you can afford it, pay down your credit cards in full on time, every time. Not only does this improve your credit utilization and ups your score, paying in full also saves you a ton in interest payment.

- Consider a debt consolidation plan – When you’re paying multiple bills from multiple credit card companies, debt consolidation could help you manage your debt. It helps reduce interest rate on the debt and lowers monthly payment. While this strategy could cause your credit score to drop, as long as you make on timely payments, your score can quickly recover. To know more about debt consolidation, call Financial Rescue’s customer reps. We can help you get out of debt and achieve a healthy credit.