")

Taking out a small loan won’t hurt. Maybe not. But when you fail to pay on time or in full, it could turn into a financial nightmare. Accumulating fees and penalties can inflate your debt, trapping you in a relentless cycle. This is the classic debt trap.

Borrowing from Peter to pay Paul

A debt trap is a situation where you find yourself caught in a cycle of borrowing and repaying debt that becomes increasingly difficult to escape. This is how it usually develops:

- Accumulating Debt: You take out a loan or credit to cover expenses or repay existing debt.

- High Costs: The new debt often comes with high interest rates, fees, or other costs that make it hard to pay off.

- Minimum Payments: You might only be able to make minimum payments, which primarily cover interest rather than reducing the principal amount.

- Growing Balance: As interest and fees accumulate, your total debt balance increases, making it harder to pay off the original loan.

- Repeated Borrowing: To manage ongoing financial pressures, you may end up borrowing more to make payments or cover new expenses, further entrenching yourself in debt.

Life events such as losing a job, incurring medical bills, or taking on more debt than you can handle can make you especially vulnerable to falling into this trap.

Debt in numbers

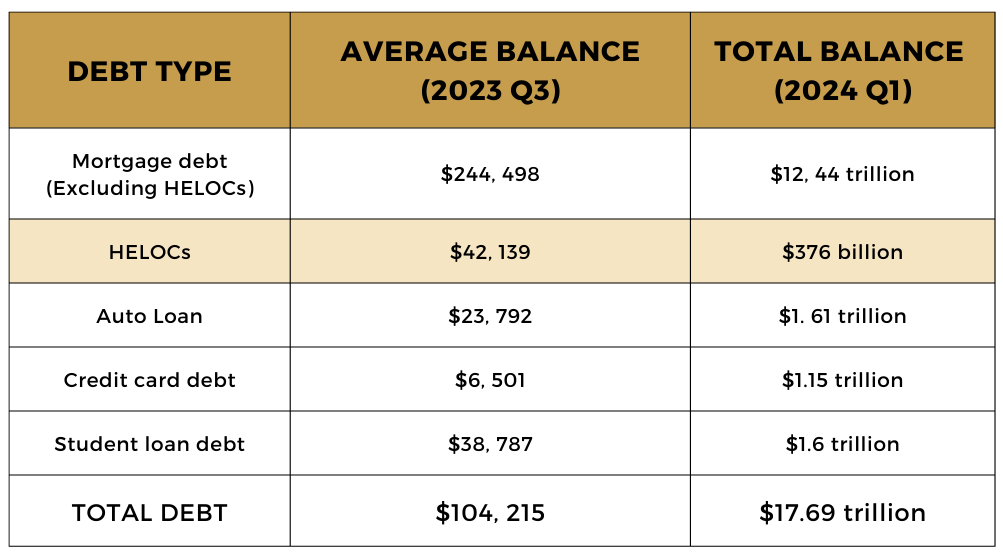

As of the second quarter of 2024, the average American household debt reached an all-time high of $104,215. This includes debt from mortgages, auto loans, credit cards, student loans, home equity lines of credit, and personal loans. Notably, mortgage debt accounts for 70% of this figure.

Source: Business Insider

Source: Business Insider

Avoiding the trap

Falling into a debt trap can take its toll not only on your credit score, but also your overall wellbeing. To avoid this, it's crucial to manage your finances wisely and make timely payments. Here’s how:

Create a Budget: Develop a detailed budget to track your income, expenses, and savings. This helps you live within your means and allocate funds wisely.

Build an emergency fund: Save an amount equal to at least 6 months of your salary. This cushion can help you navigate temporary financial crises without needing to borrow.

Consolidate loans: If you have multiple loans with varying interest rates, consolidating them into a single loan can simplify repayment and potentially reduce overall costs.

Avoid Unnecessary Debt: Only borrow money when absolutely necessary and avoid high-interest loans and credit cards unless you can pay off the balance in full each month.

Pay on time: Pay your bills and debt obligations on time to avoid late fees and penalties, which can increase your debt.

Prioritize Debt Repayment: Focus on paying off high-interest debt first and avoid accumulating new debt while you're still managing existing obligations.

Use Credit Wisely: If you use credit cards, try to pay off the balance each month to avoid interest charges. Keep your credit utilization ratio low.

Seek Professional Advice: If you're struggling with debt, consult a financial advisor or credit counselor for guidance and strategies tailored to your situation.

Stay Informed: Educate yourself about personal finance and debt management to make informed decisions and avoid common pitfalls.

By adapting these practices, you can maintain better control over your finances and reduce the risk of falling into a debt trap. If you’re feeling overwhelmed by debt, don’t hesitate to seek help. Contact Financial Rescue’s customer representatives for personalized assistance on the path to financial freedom.