Introduction

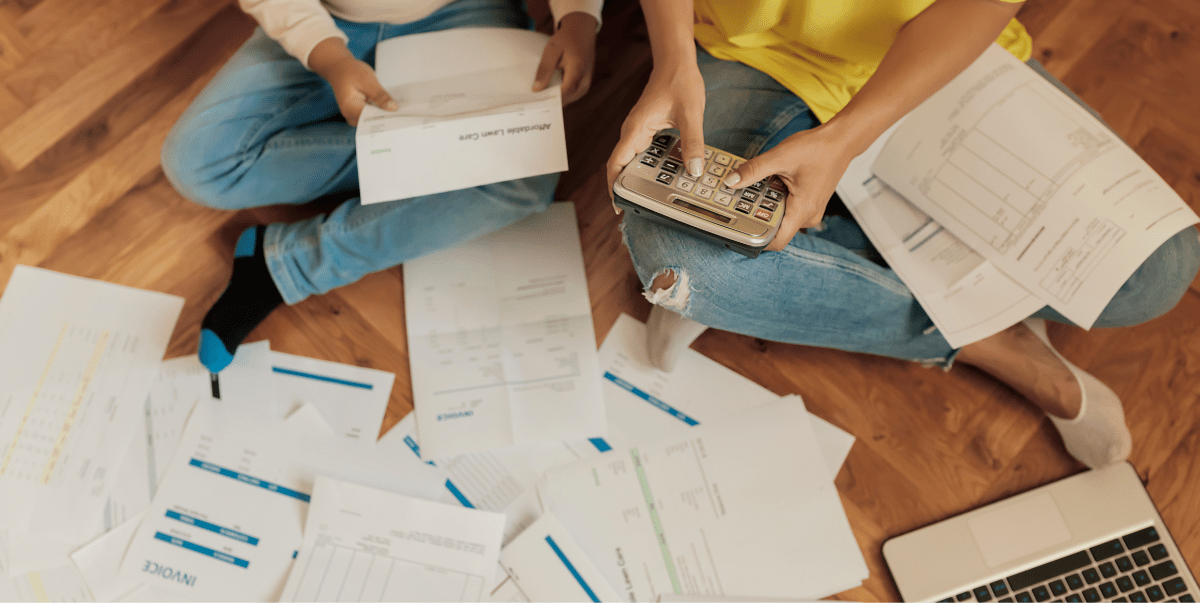

For many Filipino-Americans in the U.S., managing debt has become more challenging in recent years due to rising living costs, higher interest rates, and unexpected financial pressures. Credit cards, personal loans, and everyday expenses can quickly build up, making it harder to stay on track.

If you’ve ever felt like your monthly payments are not making a real difference, you’re not alone. This is often the point where people start exploring debt settlement as a possible solution.

But how does it actually work in 2026? And more importantly—does it still make sense in today’s financial environment?

In this guide, we’ll break down exactly how debt settlement works, what has changed in recent years, and what borrowers need to know before making a decision.

What Is Debt Settlement?

Debt settlement is a financial strategy where you or a representative negotiates with creditors to reduce the total amount of unsecured debt you owe.

Instead of paying the full balance, creditors may agree to accept a lower lump-sum payment or structured reduced settlement amount.

Common types of debt included:

- Credit card debt

- Personal loans

- Medical bills

- Certain collection accounts

It does not typically include secured debt like mortgages or auto loans.

How Debt Settlement Works in 2026

While the core process remains similar, 2026 has brought more digital tools, stricter creditor policies, and faster communication systems. Here’s how the process typically works today:

Step 1 – Financial Assessment

The first step is evaluating your financial situation.

You’ll typically review:

- Total outstanding debt

- Monthly income and expenses

- Current hardship level

- Ability to make reduced payments

👉 Internal link suggestion: “Free Debt Evaluation / Consultation Page”

This helps determine if debt settlement is the right fit for your situation.

Step 2 – Setting Up a Dedicated Account

Instead of paying creditors directly, you may be advised to set up a dedicated savings account.

Purpose of this step:

- Build funds for settlement offers

- Show financial hardship to creditors

- Prepare for lump-sum negotiations

This phase requires consistency and discipline.

Step 3 – Stopping or Reducing Payments to Creditors

In many cases, payments to creditors are paused or reduced during negotiations.

This is where things can feel stressful, but it is part of the strategy used to encourage settlement discussions.

What may happen:

- Accounts may become delinquent

- Credit score may temporarily drop

- Collection calls may increase

This is an expected part of the process—not a failure.

Step 4 – Negotiation with Creditors

Once enough funds are accumulated, negotiations begin.

Creditors may agree to:

- Reduce total balance owed

- Waive late fees or penalties

- Accept a lump-sum settlement or structured payments

In 2026, many negotiations are now handled faster through digital communication systems and automated creditor review platforms.

Step 5 – Making the Settlement Payment

Once an agreement is reached, you pay the negotiated amount.

After payment:

- The account is marked as settled

- Remaining balance is forgiven (depending on agreement)

- You begin rebuilding financial stability

Step 6 – Rebuilding Financial Health

Debt settlement is not the end—it’s a reset point.

After completion, many people focus on:

- Rebuilding credit

- Creating emergency savings

- Improving budgeting habits

Benefits of Debt Settlement in 2026

When used correctly, debt settlement can offer meaningful relief from overwhelming financial pressure.

Key benefits:

- Reduced total debt balance

- Faster path to becoming debt-free

- Lower monthly financial burden

- Structured resolution plan

For many families, this creates breathing room to regain stability.

Risks and Important Considerations

Debt settlement is not a one-size-fits-all solution. It’s important to understand the trade-offs.

Potential risks include:

- Temporary credit score impact

- Possible tax implications on forgiven debt

- Collection activity during negotiation period

- Not all creditors may agree to settle

Understanding both sides helps you make an informed decision.

Real-Life Scenario (Example)

Maria, a Filipino-American working in healthcare, accumulated $25,000 in credit card debt after medical emergencies and rising household costs.

She was only able to make minimum payments, but the balance barely moved.

After enrolling in a debt settlement program:

- She stopped adding new debt

- Built settlement funds over time

- Negotiated reduced balances with creditors

- Paid off her accounts at a significantly lower total amount

While her credit score dropped initially, she regained financial stability within a few years.

Is Debt Settlement Right for You?

Debt settlement may be worth considering if:

- You are behind on payments or struggling to keep up

- Your debt feels unmanageable even with budgeting

- You cannot qualify for consolidation loans

- You are seeking a structured exit strategy

If you are still current on payments and can manage your balances, other options may be more suitable.

Why 2026 Is Different for Debt Relief

The debt landscape has evolved significantly.

In 2026:

- Creditors use more automated collection systems

- Settlement timelines are often more streamlined

- Financial hardship programs are more structured

- Consumers have more access to digital financial tools

This makes education and proper guidance more important than ever.

Final Thoughts

Understanding how debt settlement works in 2026 gives you a clearer picture of your options when facing financial pressure. While it is not a quick fix, it can be a structured path toward resolving overwhelming debt and rebuilding stability.

For many Filipino-American families balancing responsibilities and rising costs, the key is not ignoring the problem—but addressing it early with the right information and support.

Call to Action

If you’re feeling overwhelmed by debt and want to understand your options, we’re here to help.

Contact us today for a free consultation to review your situation and explore whether debt settlement is the right path for you. No pressure—just clear guidance and real solutions to help you move forward.

Disclaimer: The content provided is for informational purposes only and should not be interpreted as financial, legal, or tax advice. Information is derived from multiple sources deemed reliable but is not guaranteed for accuracy or completeness. Financial Rescue does not assume liability for any actions taken based on this content. Outcomes may vary depending on individual circumstances. Please consult with a qualified professional before making financial decisions.