")

Debt settlement can be a significant relief, providing a fresh start for individuals burdened with overwhelming debt. However, completing a debt settlement program is only the first step toward financial recovery. Rebuilding your financial future requires careful planning, disciplined financial habits, and a commitment to restoring your creditworthiness. Here’s a comprehensive guide to help you navigate the journey towards financial stability and a healthier credit score after debt settlement.

Understand Your New Financial Situation

- Assess Your Current Financial Status

After debt settlement, it's essential to get a clear picture of your financial situation. Start by creating a comprehensive list of your income, expenses, and any remaining debts. This will help you understand your cash flow and identify areas where you can make adjustments.

- Create a Realistic Budget

A well-planned budget is the cornerstone of financial stability. List all your monthly income sources and categorize your expenses into fixed (e.g., rent, utilities) and variable (e.g., groceries, entertainment). Ensure that your budget is realistic and allows for some flexibility to handle unexpected expenses.

Rebuild Your Credit Score

- Check Your Credit Report

After settling your debts, it's crucial to check your credit report to ensure all settled accounts are accurately reported. You can obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year via AnnualCreditReport.com.

- Dispute Any Errors

If you find any discrepancies or errors on your credit report, dispute them immediately. Incorrect information can negatively impact your credit score, so it's essential to address these issues as soon as possible.

- Start with a Secured Credit Card

Secured credit cards are an excellent tool for rebuilding credit. These cards require a security deposit, which typically serves as your credit limit. Use the secured card responsibly by making small purchases and paying off the balance in full each month.

- Consider a Credit-Builder Loan

Credit-builder loans are designed to help individuals improve their credit scores. These loans work by placing the borrowed amount into a savings account that you cannot access until you've repaid the loan. Timely payments are reported to the credit bureaus, helping to rebuild your credit history.

- Make All Payments On Time

Consistently making on-time payments is one of the most critical factors in rebuilding your credit. Set up reminders or automatic payments to ensure you never miss a due date.

Establish Healthy Financial Habits

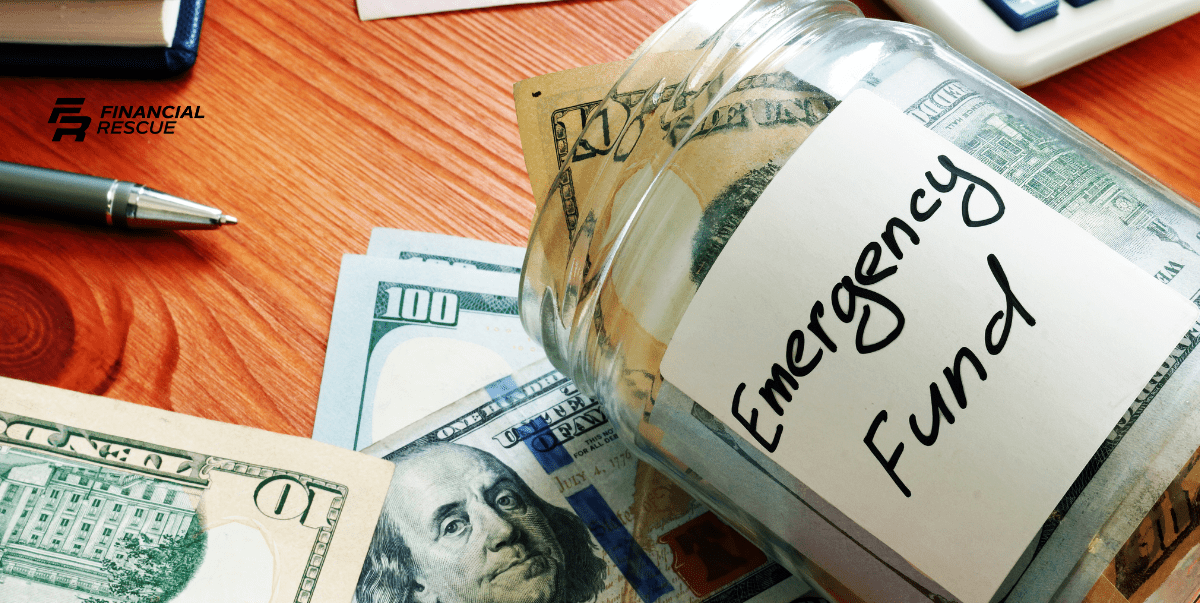

- Build an Emergency Fund

An emergency fund provides a financial safety net for unexpected expenses, such as medical bills or car repairs. Aim to save at least three to six months' worth of living expenses. Start small if necessary and gradually increase your savings over time.

- Avoid Taking on New Debt

While it may be tempting to use credit again, it's essential to avoid taking on new debt during the rebuilding phase. Focus on living within your means and using cash or debit for purchases whenever possible.

- Monitor Your Credit Regularly

Regularly monitoring your credit helps you stay on top of your credit status and identify any potential issues early. Consider using a credit monitoring service to receive alerts about changes to your credit report.

- Educate Yourself About Personal Finance

Improving your financial literacy can significantly impact your financial health. Read books, attend workshops, or take online courses to learn about budgeting, saving, investing, and managing credit.

Re-establish Financial Stability

- Set Financial Goals

Setting clear financial goals can provide motivation and direction. Whether it's saving for a down payment on a house, building an investment portfolio, or simply achieving a certain credit score, having specific targets can help you stay focused and disciplined.

- Plan for Retirement

It's never too early to start planning for retirement. Contribute to retirement accounts like a 401(k) or an IRA to ensure you have a secure financial future. Take advantage of employer-matching contributions if available.

- Diversify Your Income Streams

Having multiple income streams can provide financial stability and help you achieve your financial goals faster. Consider side hustles, freelance work, or investments to supplement your primary income.

Seek Professional Help if Needed

- Consult a Financial Advisor

If you're unsure about managing your finances post-settlement, consider consulting a financial advisor. A professional can provide personalized advice and help you develop a comprehensive financial plan.

- Join a Support Group

Debt settlement can be a stressful experience. Joining a support group can provide emotional support and practical advice from others who have been through similar situations.

Protect Your Financial Future

- Review Your Insurance Coverage

Ensure that you have adequate insurance coverage for health, home, auto, and life. Proper insurance can protect you from financial setbacks due to unexpected events.

- Keep Important Documents Organized

Maintain a system for organizing important financial documents, such as tax returns, bank statements, and insurance policies. Keeping these documents organized can help you manage your finances more effectively.

- Plan for Taxes

Understand the tax implications of your debt settlement. Sometimes, forgiven debt may be considered taxable income. Consult with a tax professional to ensure you comply with tax regulations and to explore any deductions or credits you may be eligible for.

Conclusion

Rebuilding your financial future after debt settlement is a journey that requires patience, discipline, and strategic planning. By assessing your financial situation, creating a realistic budget, rebuilding your credit, and establishing healthy financial habits, you can pave the way towards long-term financial stability. Remember, the key to success lies in taking consistent, small steps towards your financial goals. Stay committed to your plan, seek professional help if needed, and celebrate your progress along the way. With determination and the right strategies, you can successfully rebuild your financial future and enjoy a more secure and prosperous life.