Still reeling from holiday expenses? Get your finances organized and your money goals on track. There’s no better time to do it than at the start of the year. All it takes is 5 easy steps.

1.Prepare a budget

According to the American Institute of CPAs’ National CPA Financial Literacy Commission, making a budget should be at the top of your list when you want to take control of your finances. This means mapping out your bank accounts, your fixed expenses, expected income, your savings goals as well as your outstanding debts.

To find out what debts you owe – credit cards, personal loans, mortgages and more – you can obtain one free copy of your credit report every 12 months by visiting AnnualCreditReport.com. You may get your credit reports from the three major credit bureaus: Experian, TransUnion and Equifax.

2. Pay off your debts

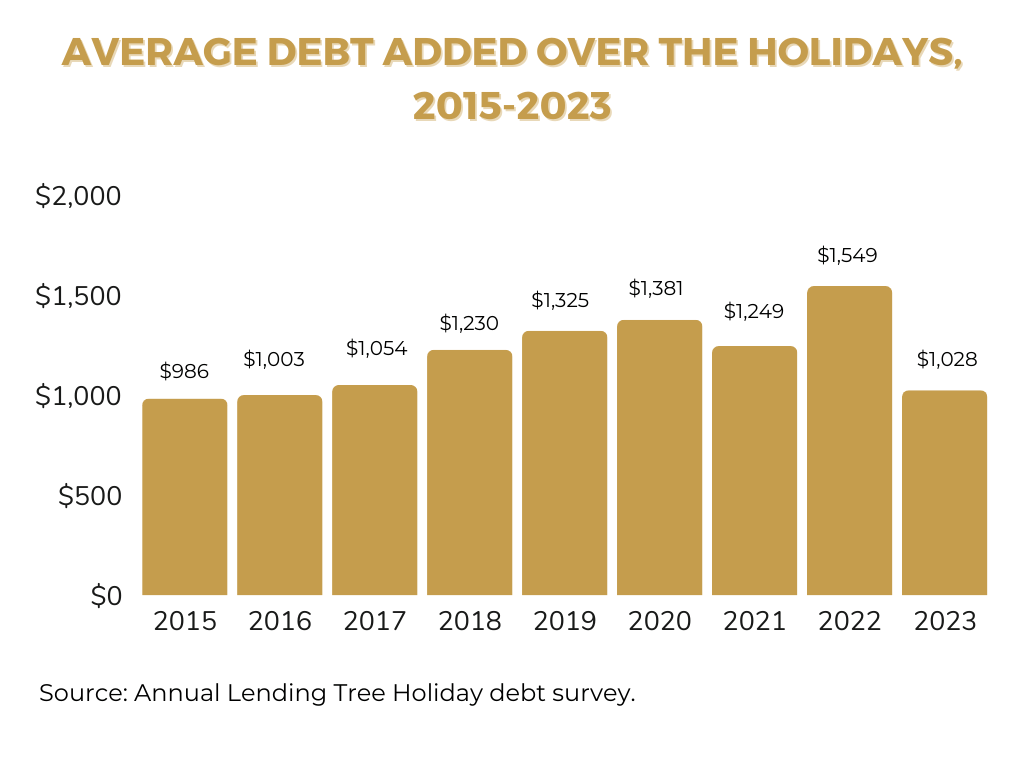

Along with holiday spending comes big credit card bills. According to the latest LendingTree survey of nearly 2,000 U.S. consumers, 34% of Americans went into debt over the holidays last year with an average debt of $1,028. While this is 34% lower than last year’s average of $1,549, majority of those who went into debt used credit cards, paying interest rates of 20% or higher.

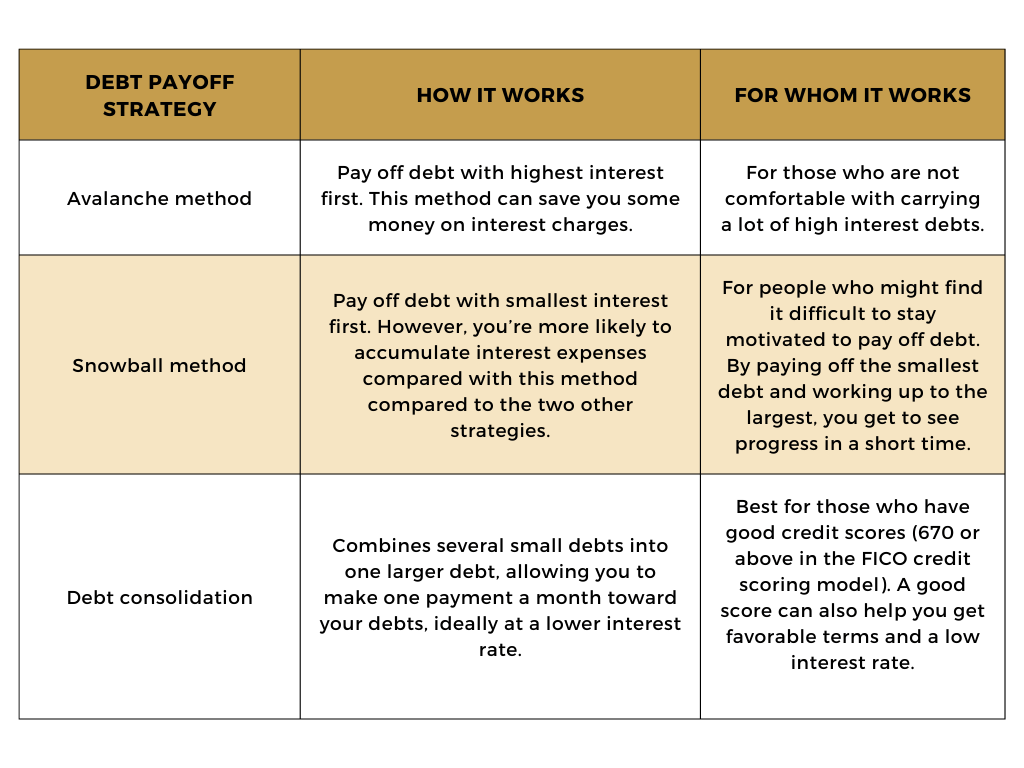

The good news is you can take control of your debt by using any of these 3 strategies

If you think debt consolidation is for you, get expert advice from Financial Rescue’s customer service. Give us a call and we can walk you through the debt consolidation process.

3. Automate your savings and spending plans

Stick to your budget by leveraging technology to pay your bills or to regularly set aside money for your savings or investment. By automating these processes, you won’t miss out on your due dates and develop a more disciplined approach to building your nest egg.

4. Set your savings goals

It’s not enough to simply save more money. Before you even start saving, identify your short, medium- and long-term goals. For example, set up an emergency fund where part of your paycheck is regularly deposited. So when some emergency happens, you can pull out funds from your emergency savings instead of resorting to expensive options like using your credit card. Then for your medium-term goals, have a sinking fund where you can set aside small monthly increments to pay for future expenses like vacations, home improvements, medical needs. And finally for your long-term goals, create a retirement savings by saving 15% of your income. By identifying your savings goals, your savings strategy becomes more focused and disciplined.

5. Identify financial issues

Find out what makes your finances go off kilter. Are you spending too much on your groceries? Does your insurance policy come with unnecessary features you’ve been paying for? Are you overspending on your credit card?

Being mindful about these financial issues puts you in better position to take control of your finances. Here’s to turning 2024 into a year of real growth and financial freedom!